2 hours ago

1

2 hours ago

1

Sasol’s share price jumped nearly 12% to R118 on Monday, after the fuel and chemical group announced its results for the financial year to end June 2025. The share has more than doubled since its low of around R55 a few months ago.

President and CEO Simon Baloyi and CFO Walt Bruns told shareholders in a presentation that the results demonstrate “clear progress in delivering against the strategy and commitments” promised earlier in 2025, when Sasol shared its plans for the next few years with stakeholders.

Listen/read: Sasol’s plans to boost fuel production and expand renewables

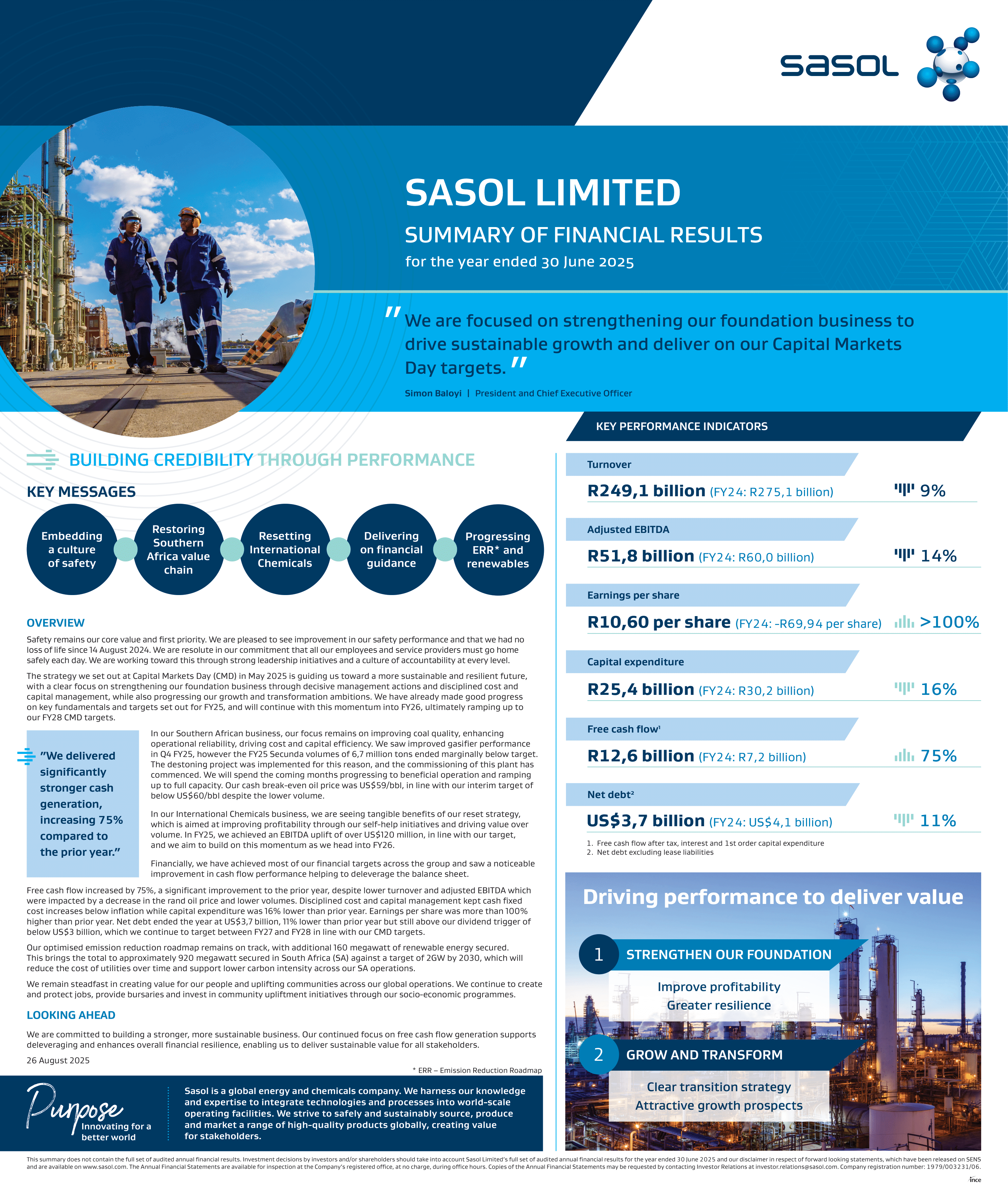

“Sasol delivered a strong cost performance and disciplined capital management, resulting in 75% higher free cash flow compared to the prior year, despite a challenging macroeconomic and operating environment.

“Financial year 2025 has been a pivotal year for Sasol, as we mark our 75th anniversary and pursue our future with renewed purpose and a clearly defined strategy,” said Baloyi.

“We outlined a clear set of deliverables for the 2028 financial year, which were to restore the reliability and competitiveness of our SA value chain, drive margin improvement in our international chemicals business, and advance our growth and transformation agenda in a manner that enhances value.

“We also committed to de-leverage our balance sheet through free cash flow generation and disciplined capital allocation. Today’s results show that we are beginning to deliver on those promises,” said Baloyi.

Cash flow

A feature of the results was the very strong cash generation, albeit aided by an unusual cash inflow of R4.3 billion in the form of a settlement of a legal dispute with state rail operator Transnet. Another unusual item – a decrease in the provision for rehabilitation costs of nearly R3 billion compared with the prior financial year – also benefited cash flow.

Bruns said that the results and, in particular, the improvement in cash flow, show that margins have improved. This was achieved by containing the increase in cash costs by only 1%. In addition, capital spending reduced.

“These actions are building greater resilience in our business. Importantly, it gives us confidence that we will reach our net debt target of below $3 billion by 2027 or 2028, enabling us to reinstate dividends and support investment in future growth and transformation.

“Sasol reduced its net debt to $3,7 billion, the lowest level since 2016 and 8% lower than our target of $4 billion at the end of the 2025 financial year,” said Bruns.

The cash flow statement shows that free cash flow (after tax, interest and first order capital expenditure) increased by 75% to R12.6 billion.

Bruns said that the macro-environment in which Sasol operated in the last year was highly volatile, influenced by uncertainty around global tariffs and heightened geopolitical tensions.

“These dynamics have had varied impacts across our business segments. In our fuels business, a 15% lower rand-oil price and 68% lower refining margin had a significant negative impact on its results.

“Meanwhile, our chemical segments benefited from a stronger ethylene margin in the US and a 5% improvement in the chemical basket price,” he said.

Undervalued

Basic earnings per share increased by more than 100% to R10.60 per share, compared with a loss per share of R69.94 in the prior financial year. Headline earnings per share nearly doubled to R35.13, placing the share of a price to earnings ratio of 3.4 times.

Shaun Murison, senior analyst at Rand Swiss, says that Sasol has been undervalued for a long time and that the good results might help to push the share price still higher.

“There were a lot of positives in the results. We saw a solid growth in free cash flow of 75% and the reduction in debt will help to strengthen the balance sheet.

“Cost increases were kept well below inflation and capital expenditure is starting to decrease. While earnings grew substantially, it should be noted that the increase was largely due to the lower impairments from a high base of comparison in the prior year.

“The Transnet settlement was also another one-off item boost to earnings,” he says.

Murison noted that there are still a few things that might bother shareholders.“One of the negative factors to consider is that Sasol decided not to pay a dividend yet, and that total debt still remains above the targeted threshold.

“Sales volumes were lower, and macro-economic conditions are expected to remain tough,” he says.

Nonetheless, Murison believes that the market is optimistic about the turnaround story. “We are seeing that reflected in the price.

“Analysts’ target prices have, for a while, suggested that Sasol was undervalued around recent levels. The net positive results will help to narrow the gap between the share price and analysts’ fair value targets,” he says.

Sasol management promises that the group will continue to improve.

Baloyi said: “We know there is more to do, but we are clear on the strategic path ahead, to strengthen the foundation, unlock value and drive our transition.

“The actions taken this year have laid the groundwork, with positive momentum across the business. We will continue to build on this in the years ahead.

“Our long-term ambition remains unchanged: to build a stronger, more sustainable Sasol that creates value for our stakeholders, including shareholders, people and society.”

View the results summary here.

Brought to you by Sasol.

Moneyweb does not endorse any product or service being advertised in sponsored articles on our platform.

English (US) ·

English (US) ·