5 hours ago

1

5 hours ago

1

At first glance, Clicks Group (CLS) and Dis-Chem Pharmacies (DCP) appear similar.

Both operate retail pharmacies around South Africa, both have seen their share prices perform well, and both have high valuations relative to the rest of the market – a 30 times price-earnings (PE) ratio for Clicks, and a 23 times PE for Dis-Chem.

ADVERTISEMENT

CONTINUE READING BELOW

Read:

Clicks cashes in on health and beauty demand

Dis-Chem delivers 20% profit surge on back of payroll cost control

But the differences between the two start to become a little more apparent once you dig deeper.

Clicks is older, has a large store network, and its store footprint focuses more on smaller format, convenience retail stores with pharmacies.

On the other hand, Dis-Chem has traditionally built out large-format retail stores with pharmacies – although this focus does appear to be shifting

Both retailers place the dispensaries at the back of the stores to get customers to walk through the store and hopefully buy other items en route.

Another operational difference is the Clicks ClubCard loyalty programme, which accounts for around 82% of its sales to 12.1 million active customers, while Dis-Chem’s loyalty programme is a lot less developed.

Read: Loyalty programmes on the rise in a shifting economy

Likewise, Clicks’ private label products make up around 27% of its sales (its target is to get to 35%), while Dis-Chem’s private label offering appears to have much lower penetration (it does not specifically disclose these figures).

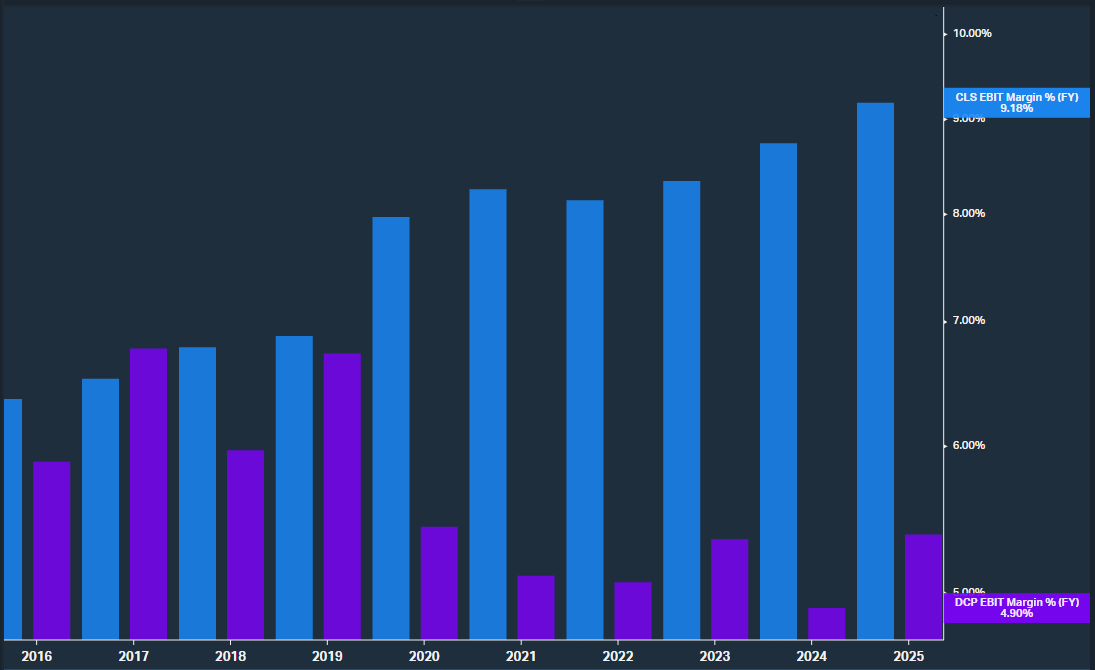

Some of this comes through in Clicks’s superior earnings before interest and taxes (Ebit) margin.

Clicks versus Dis-Chem – operating profit (Ebit margin), %

Source: Koyfin

In some ways, this is more a function of Clicks just being older and more mature than Dis-Chem, but it comes out in other features.

Below is Clicks and Dis-Chem’s return on equity (ROE) over the last five years, which Clicks clearly wins comfortably.

Clicks versus Dis-Chem – return on equity (ROE), %

Source: Koyfin

Interestingly, Clicks beats Dis-Chem on ROE despite having a largely ungeared balance sheet – in other words, no debt to enhance its returns – versus Dis-Chem’s net debt balance sheet.

How about a global comparison?

The world’s largest listed retail pharmacy is Walgreens Boots Alliance with a market cap of $9 billion or around R160 billion.

ADVERTISEMENT:

CONTINUE READING BELOW

The group used to be a lot bigger, but Big Pharma starting to build direct-to-consumer channels and Trump-driven attacks on medicine intermediaries have seen its share price crater by about a third in the past 12 months.

Still, Walgreens is a good benchmark against which to continue our assessment of Clicks.

I prefer return on assets (ROA) for global return measures for a range of reasons.

And, well, Clicks once again shines.

Clicks versus Walgreens – ROA (%) and Ebit margin (%)

Source: Koyfin

Clicks is more profitable and has massively higher margins.

As a convenience-based retail pharmacy, Clicks is literally the world-class pharmacy down the road in South Africa.

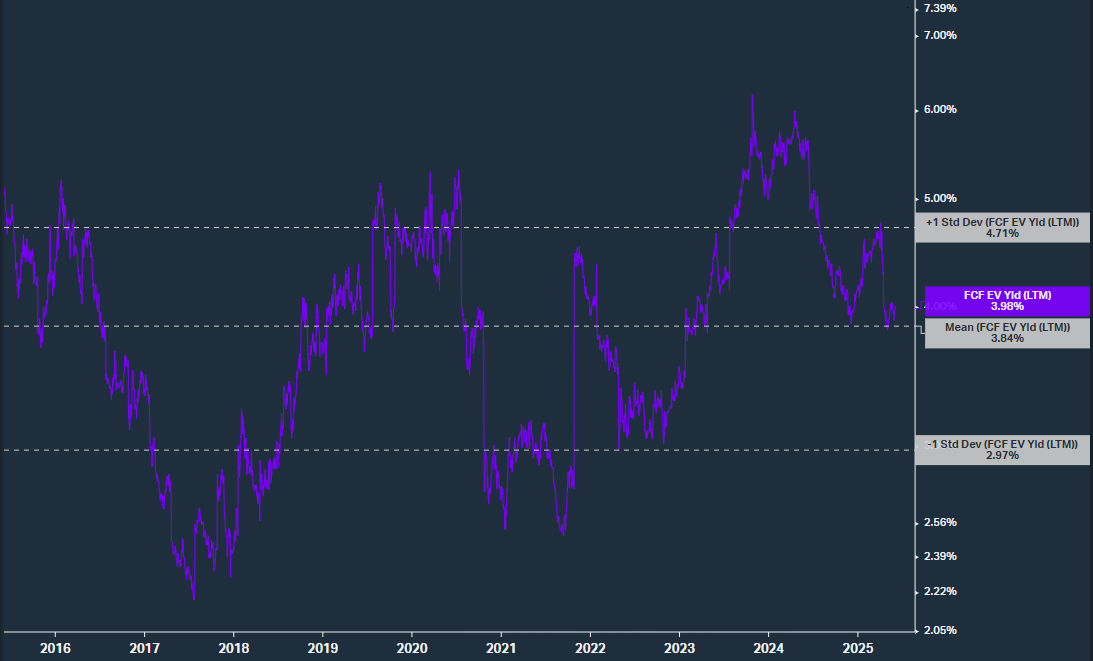

But at a 30 times PE, is it still worth investing in?

Well, if we look solely at its own history, its valuation relative to its free cash flow is more or less in line with its historical average (based on a free cash flow yield perspective and a 10-year horizon).

Clicks – free cash flow/enterprise value yield (%) versus mean and standard deviations

Source: Koyfin

Thus, simplistically, the world-class pharmacy down your road currently sees its shares trading at a mere average valuation.

Keith McLachlan is CEO of Element Investment Managers.

Follow Moneyweb’s in-depth finance and business news on WhatsApp here.

English (US) ·

English (US) ·